Estate planning 101: wills, trusts and the $1,000 Challenge

Jun 14, 2019, 1:32 PM | Updated: Oct 4, 2019, 10:35 am

Photo credit: KSL TV

![]()

This $1,000 Challenge about estate planning is Presented by Zip Mortgage powered by Zions Bank. Visit zionsbank.com. *Loans subject to credit approval; terms and conditions apply. A division of Zions Bankcorporation, N.A. Member FDIC. ![]() Equal Housing Lender. NMLS# 467014.

Equal Housing Lender. NMLS# 467014.

SALT LAKE CITY — Trusts. Wills. Assets. Estate planning. Most of us would agree it doesn’t sound like much fun, but financial experts say it’s a critical part of managing your money.

Eric Barnes, an estate planning attorney with the ElderCare Law Firm, told KSL TV the state has its own plan for what happens if you die without an estate plan in place.

“If you don’t like that plan, then you might have assets going to people that you would not have wanted them to go to,” he said.

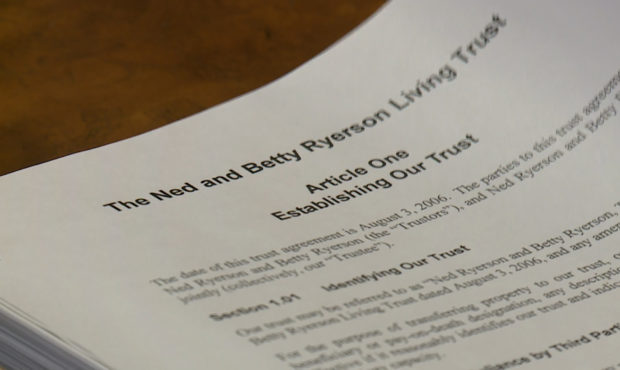

Estate planning: a will or a trust?

It’s a top reason why Barnes says everyone should have a will. But he also says if you own a home, you may want to consider also having a trust.

“A trust is more like a box that you put your assets into,” he explained, “and then the trust owns the assets instead of you as an individual.”

If something happens and you become incapacitated or you die, Barnes says a successor would then take over that box and follow the instructions you left behind. The advantage, he says, of a trust over a will is that probate court is not involved.

“It usually takes at least a minimum of 120 days to get through the probate process,” Barnes said.

In other words, with a trust, you’re able to designate who gets your assets without things becoming complicated by the court system. And, he adds, once a will goes to probate court, it becomes part of the public record — meaning anyone, including identity thieves, can see not only what it was that you owned, but who owns it now.

Additionally, Barnes says a will only takes effect in the event of your death.

“But a trust is in effect during life, and so it’s really a great vehicle to manage assets in the event of disability,” he said.

However, wills also have advantages, according to Barnes. They are simpler to set up and change, and they are less expensive than a trust. They can also name a guardian for minor children, which trusts cannot do.

Either way, Barnes advises revisiting your estate plan at least every three years — and sooner in the event of a major life event, such as a marriage, divorce or birth.

More to the story

Join the $1,000 Challenge Facebook group to see other brilliant ideas on how to get your budget in check and to be a part of a tribe that’ll encourage you every step along the way.

And tune into Dave & Dujanovic every day from 9 a.m to noon on KSL Newsradio 102.7 FM / 1160 AM for financial tips and tricks Monday through Thursday.

Dave & Dujanovic can be heard weekdays from 9 a.m. to noon on KSL Newsradio. Users can find the show on the KSL Newsradio website and app, as well as Apple Podcasts and Google Play.

![]()